Looking into how two giants across the Atlantic compare.

The previous post mentioned that almost two-thirds of US commercial banks are not members of the Federal Reserve system. Though they can still access services provided by the Fed, these banks are not subject to direct supervision from their respective Reserve bank—instead falling under local and Federal Deposit Insurance Corporation supervision¹.

This finding struck me as odd. For one, minimum reserve and other requirements are not homogenous between members and non-members. Regulations for non-member banks can also be less strict.

Allowing banks to be non-members in the US seems to add an unnecessary level fragmentation for banking supervision. Try comparing that to the eurozone (that has standardised MRR across countries), where there are talks about even implementing a banking and capital markets union. This subtle difference in how the systems operate prompted me to look further into the decentralised nature of the Federal Reserve System (yes, two Fed posts in a row!)

One key difference between the operational frameworks of the ECB and the Fed is that the latter provides liquidity mainly through asset purchases. Such open market operations can offer a much more targeted and time-effective alternative to traditional standing facilities. Lending operations to banks still of course exist for commercial banks to use at their own discretion.

With that being said, I was curious to learn if not relying enough on bank lending directly from the central bank weakened the strength of its interest rates (here the Federal Funds rate). After all, these are the interest rates that cause a ruckus every six weeks or so when the Open Market Committee decides on whether to change them.

To test this, I compare average changes in different market interest rates from 1999 onwards in quarters preceding, during and following interest rate decisions (rise, decrease or remain unchanged). The fact that rate decisions come in monetary policy cycles lasting from months to years accounts for a lag in the transmission mechanism (e.g. rate increases come in successive spells lasting a mean of almost two years for the Fed).

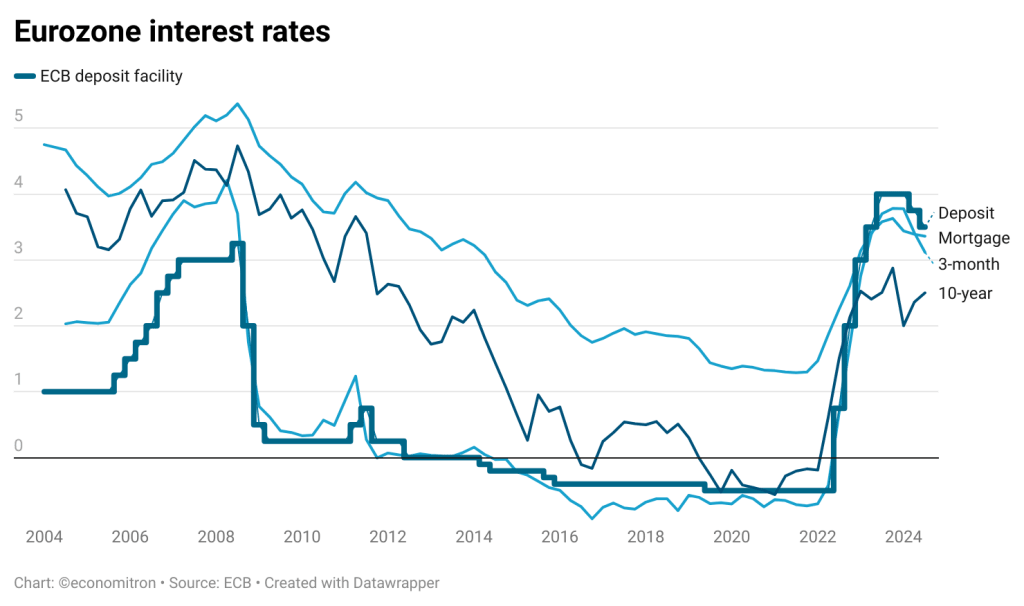

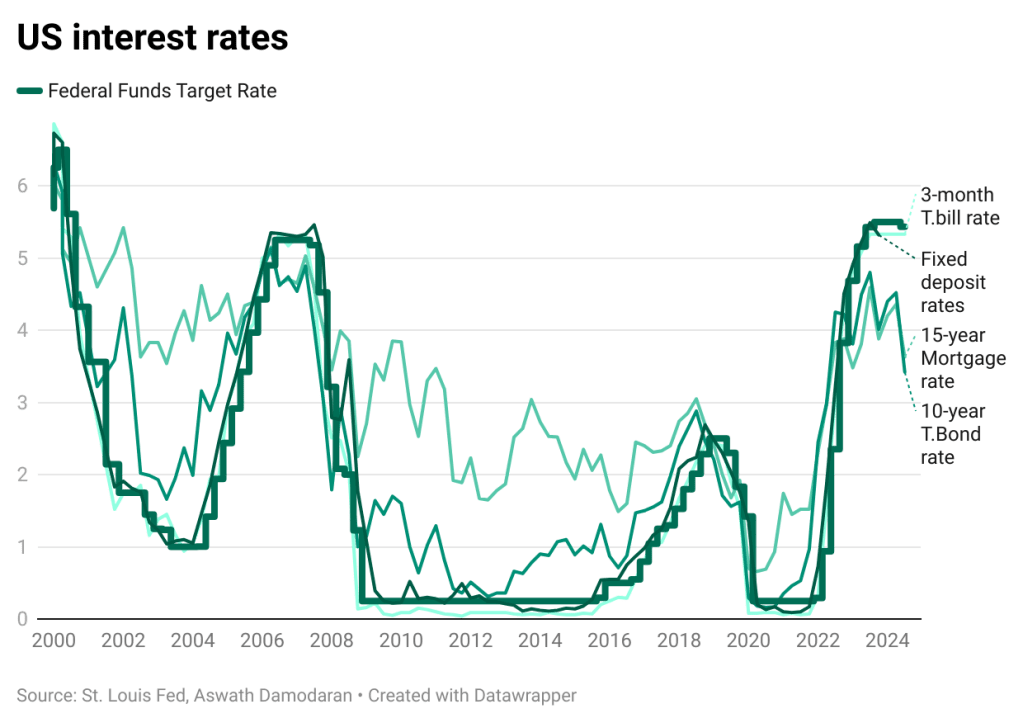

The idea is based on a similarly spirited data analysis by Aswath Damodaran, professor at NYU. In theory, the more aligned market interest rates are with decisions, the stronger the central banks’ transmission mechanism’s pass-through is. I also include data for the ECB—where the assumption is that its interest rate decisions are more influential in driving monetary policy—to test the hypothesis.

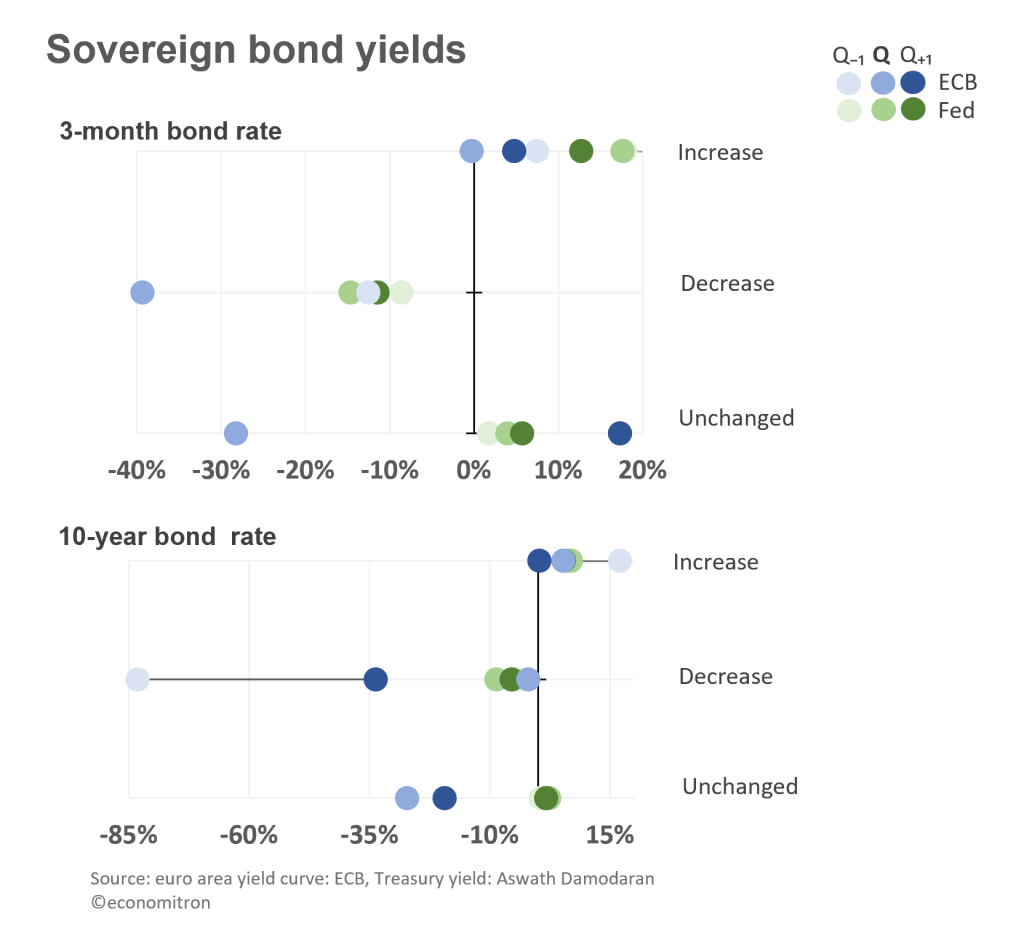

First up, sovereign bond yields—both Treasury and euro area government bonds for the Fed and ECB respectively. We look at short-term and long-term rates. For reference, bond yields and interest rates are expected to have a direct relationship.

The data are interesting in several aspects. Firstly, it seems as though short-term bonds have been very reactive to ECB rate cuts. There have been an almost equal number of cuts and rises, for reference. However, all other short-term rate decisions seem to be more aligned with the Fed. Long-term rates, on the other hand, have shown to be far more responsive to changes in the ECB’s key interest rates. We’ll call this a tie between the two.

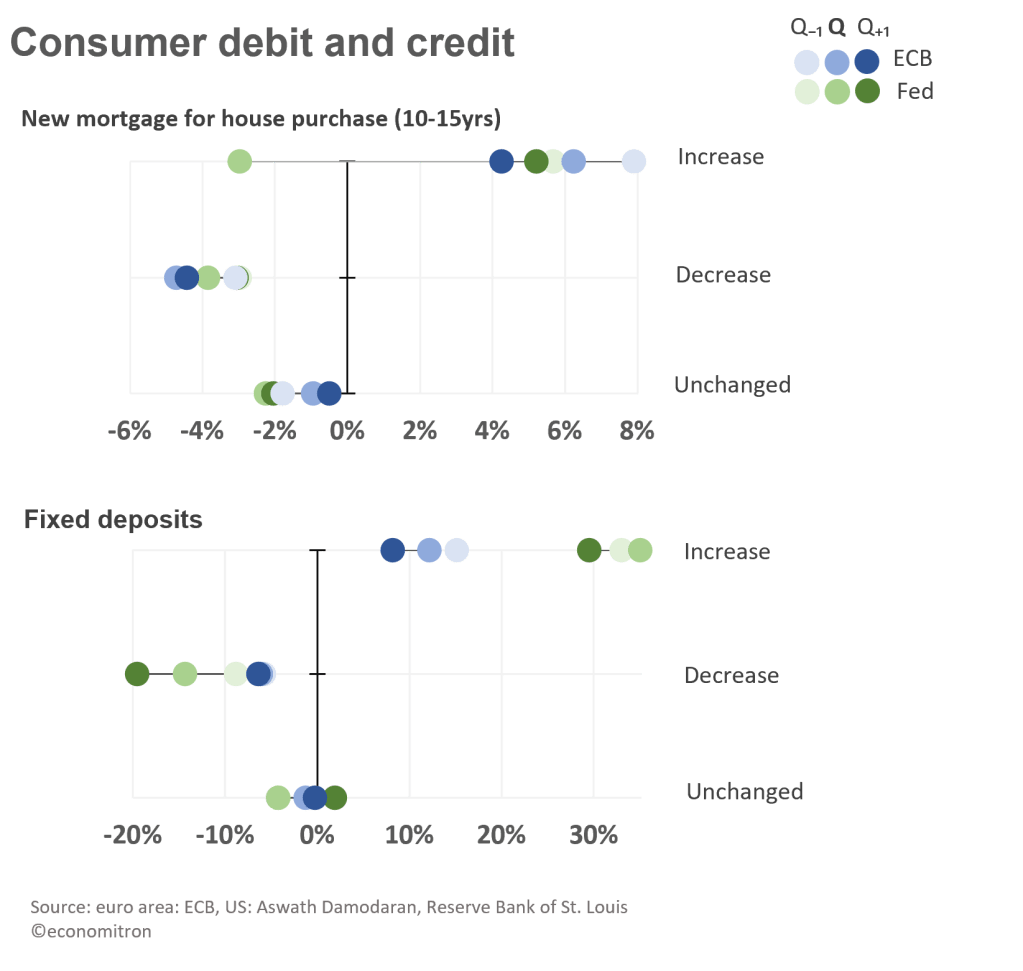

Lastly, we’ll look at consumer interest rates, here represented as the rate of mortgages as well as of deposits with a fixed maturity. As can be expected, long-term mortgages are far less responsive to interest rate decisions than any of the other rates. The ECB seems to eke out the Fed here, with ever-so-slightly stronger pass through for all rate decisions. Deposit rates, however, strongly favour the Fed. Another tie!

So, what conclusions can be drawn from this? For one, it appears that market rates are closely aligned to both central banks’ key interest rates. Only one case (Fed rate hike’s effect on mortgages) displayed explicit defiance towards central bank rate decisions. Neither central bank appears to have a stronger transmission mechanism based on the results, so a tie all-around!

As for the age-long question on whether central banks are rate leaders or followers (i.e. setting the market rate as opposed to following the tide and yielding to expectations), the answer is less clear: in some instances, quarters preceding rate decisions showed the strongest change, whilst in others the impact was most pronounced on the quarter itself or directly following it. Placing the interest rates on a time scale does not provide much help either. Whether or not markets align with interest rates or they align to markets is going to be a question for another day.

As for Fed decentralisation, whilst interest rates have proven to be effective (meaning that the peculiar membership model does not seem to affect monetary policy), the axis of banking supervision and financial stability still needs to be unravelled. For instance, the rise in non-banking institutions and private credit levels—which are especially pronounced in the US—represent a concerning source of systemic risk that spans beyond the central bank’s control. That too is a topic for another day.

Interest rates: bad news for those saving to buy a house, a source of endless entertainment and debate for those anticipating rate decisions. This analysis has shown that central bank rates do in fact align with market interest rates, placing equal strength to both Fed and ECB rate decisions. So, love them or hate them, interest rates as a tool for monetary policy are here to stay.

Leave a comment