With the turn of the year, Bulgaria has become the latest member to join the eurozone. The question remains: are political aspirations superseding economic soundness?

This blog has previously argued for a strong and deepened Europe, and for unison in the face of adversity. The currency area, now made up of 21 member states, represents the best example of such economic integration. It facilitates both intra- and extra-EU trade and enhances stability for businesses and citizens. Besides being an obligation as an EU member state, Bulgaria’s accession into the eurozone is a milestone in its decades-long trajectory towards the West. It is meant to represent a step away from corruption and into the ideals of the larger European family.

The value of economics comes in its ability to disentangle ideology from reality. Half of Bulgaria’s population opposes the country’s adoption of the euro. Many well-founded concerns remain, and left unaddressed, scrutiny against integration ignored for the sake of integration risks undermining the very benefits it aims to bring.

Adopting a common currency between countries ties into the idea of an Optimum Currency Area. Adhering to a one currency is appropriate for countries that see free trade of goods & services (Friedman) and have similar economic fundamentals. The second point is not a footnote but crucial to maintain a union free of friction and is at the center for the concerns with Bulgaria’s accession.

The first step of accession into a currency area is convergence. The country has long been preparing for accession, having already pegged to the Euro in 2006. This has given it de facto monetary policy subordination well before it adopted the currency.

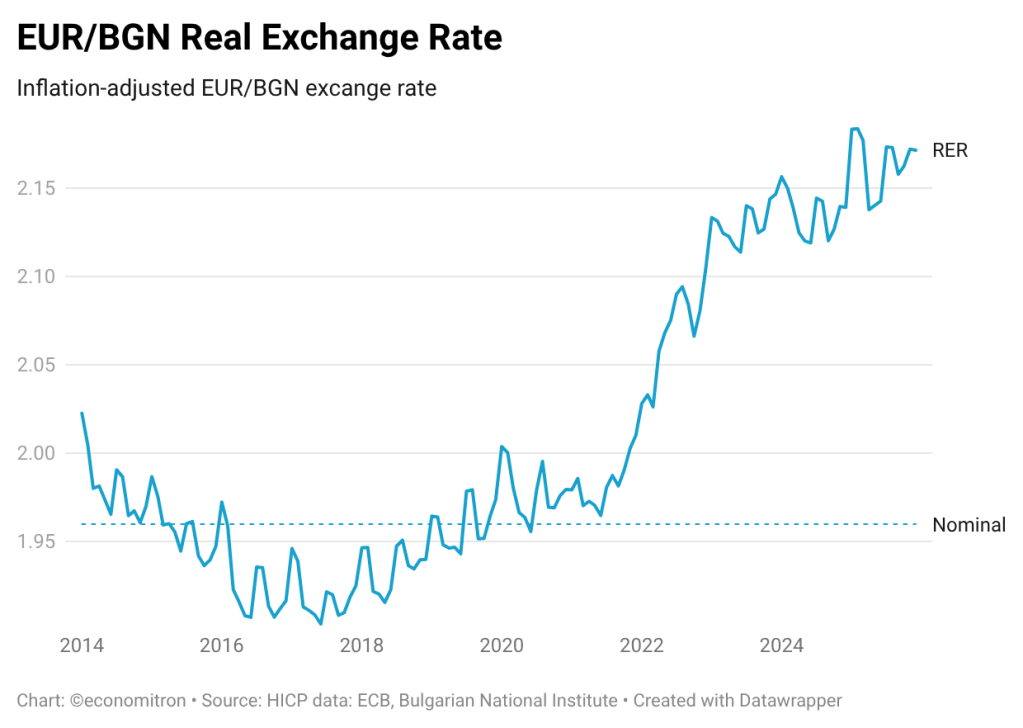

Given the expectation that Bulgaria is less economically developed than the rest of the Union, convergence outside of the union should have resulted in an appreciation of the long-run equilibrium exchange rate (the rate where external balance holds). The presumed appreciation is caused by economic development in anticipation of joining the Euro club causing productivity growth and high wages in tradeable goods, which spill over to the rest of the economy. Due to inflation and given a constant nominal exchange rate, the real or inflation-adjusted exchange rate appreciates over time.

Then the argument goes: joining a currency area comes with inflation!

Nevertheless, when Croatia became the 20th member of the eurozone in 2023, it’s price increases seemed to be both marginal and transitory. The country boasts of an economy stronger than Bulgaria in relative terms, and was able to adequately absorb the asymmetrical positive shock that comes with joining a currency area. This is despite losing the ability to rely on a nominal exchange rate appreciation to absorb positive (thus inflationary) shocks. Hence, it did not suffer from an artificially looser monetary policy regime caused by the inflation differential, which is made even worse considering that a less developed economy should be expected to have a higher real interest rate.

The latter portion could become a point of concern if Bulgaria was to experience inflation. It is safe to say that its economy would fare worse than Croatia’s against positive exogenous shocks; this is where the peg comes in. It turns out that the currency peg presents the only viable option (at least in the writer’s mind) in which accession does not result in excessive inflationary pressures. As far as external trade and balances are concerned, changing currencies adds a different label to the same product.

What this entails, however, is that Bulgarians have been paying for relatively more expensive domestic goods all along the currency peg—while forgoing the benefits of autonomous monetary policy. This is an issue for those whose wages have not benefited from the productivity growth responsible for the expensive goods. What’s more, economic theory argues that maintaining a peg will always result in a disequilibrium of the external balance in the long run, as the nominal exchange rate cannot converge to its equilibrium position. Given structural and constant appreciation, this bodes poorly for exporting industries over time.

Adopting the €uro presents a cosmetic culmination to the 20-year long peg. This cosmetic change carries the ideological undertone of more integrated cross-border payments fit for any EU member state while mitigating any new risks. However, whether the already present risks have been well distributed may be reflective of current political malaise in the country. Whilst 49% of Bulgarians decry the adoption of the Euro, the decision to adhere to the common currency was never a matter of national referendum.

Leave a comment