Starting my first module of macroeconomics has mended my love for economics, which had been put to the test by the unending bore of micro in the first semester. My main qualm with the latter (as taught by the syllabus) was the arbitrariness of the scenarios featured in its problems coupled with its unappetizingly constrained scope. Solving constrained optimisation problems is more taxing on students’ mechanical pattern-spotting skills than on their creative intuition.

A good economist cannot survive off mindless memorisation. Prior to this, my four years of experience in high school economics leaned heavily on intuition. Even with projects that went beyond the typical school curriculum, we did not have much more than a nascent but strong grasp of economic relationships to guide us. Understanding how variables interacted with each other by building an image in our minds, and adding more and more blocks to that story as time went on, was and still is the most exhilarating part of learning this social science.

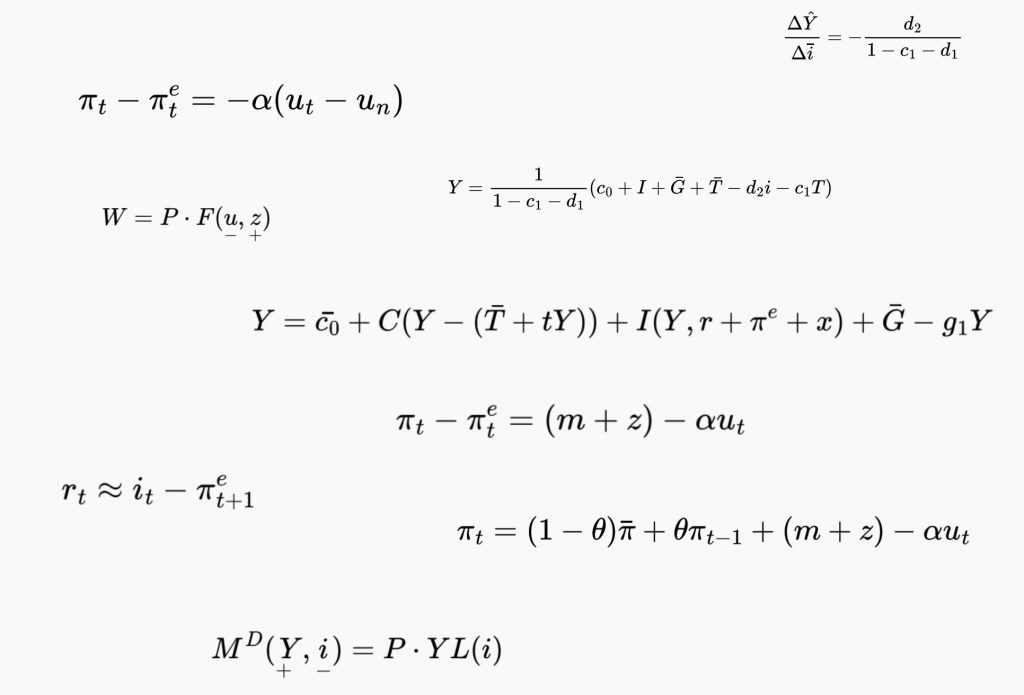

Hence came my surprise when, very early on, it became clear that macroeconomics would be taught exclusively through introducing, fine-tuning and adding to economic models. Like at times the price level P or government spending G, the boundaries we operate in are set exogenously: Olivier Blanchard’s textbook gives us the set of rules and relationships to be obeyed, and we see what happens when something is changed.

This struck me as peculiar, because no attention is given to building up the intuition necessary to understand what the relationships mean. The comparative advantage of having had the luck to already build solid foundations allows me to appreciate the value of economic models, but it also makes me question what model-heavy teaching tells us about economics.

Firstly, economic models are really, really cool. I now understand analytically many concepts that had previously been only words in essays to me. I love being able to see old things in a new, more rigorous way. I feel as if I have earned a new tool to understand or visualise better what I already knew. As of recent, I have also become better acquainted with models outside of Blanchard’s simplified textbook world; from Krugman’s first-generation model of currency crises to Bernanke’s and (again) Blanchard’s analytical characterisation of the post-pandemic inflation spike.

Models are especially cool because of their self-consistency. Their inherent simplifacation of reality, with sufficiently realistic assumptions, results in a rewarding experience when changing variables inside the model leads to the expected outcome.

But introducing maths into the social science comes with its drawbacks, naturally. Economics has always tended to move away from social sciences and into the realm of ‘hard sciences’. By modelling inflation dynamics through the flow of water in pipes, economists improve their confidence in their ability to understand variables at play while foregoing the nuance of animal spirits. If physicists can have confidence in their natural laws, then so must economists be able to find refuge in their models.

My issue with economic models is not that they are fallible or not exhaustive. Ignoring certain variables, such as international trade, allows us to better analyse first-order relationships under the mantle of ‘all else being equal’. Krugman’s, Bernanke’s and Blanchard’s models are far from complete, but they help explain the story of economic interactions whilst also leaving the door open for other papers to develop on their basis. They are useful, even if wrong.

My qualm comes when operating within mathematical variables takes precedence over intuition, the very essence of this social science. One simply cannot begin with an economic model and mold intuition around it. It is a fun intellectual exercise, not how teaching should be carried out. By teaching future economists to conform to models and to explain why something happened ex-post, the proper order of events is reversed. With this line of thinking, we regress back to the mechanical problem solving I sought to leave behind.

For instance, at university, much emphasis has been placed on sketching out a basic expression for the Phillips curve. But little effort has been allocated on covering the historical or economic foundations that led to the model in the first place. The macroeconomic system is in many ways a living being. To encapsulate it in a simple identity without properly addressing why variables are where they are is to denigrate the history behind them.

It is also destructive to economics as a science. If economists learn to breathe and think inside a box, they will be left unprepared when unexpected events happen. Indeed, many major movements in economic theory and models have been reactions to historical events—like Keynes’ neoclassical theory after the Great Depression or the resurgence of Quantity Theory of Money after the 70s’ inflation. Flexible and dynamic intuition, thereafter backed by a suitable model, is the only thing that can keep up with the forefront of real economic developments.

University macroeconomics has thus far fallen short by contributing to the illusion that there exist certainties in macro, neatly drawn out by elementary models. By prioritising the maths ahead of the intuition, we forget that the most useful indicator of our present oftentimes is our history. Whilst economic history has created the modern models, it is also full of examples of when models missed the mark—both are facts we should heed to and give credence to. In the meantime, while the syllabus remains unchanged, I will continue engaging with this very enticing fiction.

Leave a comment