The independence of our central banks (CBs) is key to modern economic systems. Having been brought to public attention through controversy around the Fed’s chair, I became curious to see if I could uncover relationships in the data that’s out there. Does the level of economic development meaningfully affect a country’s CB’s level of independence? Do better central banking institutions correlate with better inflation outcomes?

Independence in this context implies freedom from political or otherwise external pressures to act with full sovereignty over the bank’s mandate, most typically price or exchange rate stability. The leading assumption is that a higher stage of economic development should correlate with greater independence, and the latter correlates with lower average rates of inflation.

To spearhead this analysis, I use a handy index created by Davide Romelli. The variable spans from 0 to 1 in ascending degrees of independence. To accompany the analysis, I categorise all countries in the dataset between ’Low’, ’Lower-Middle’, ’Upper-Middle’ and ’High’ income countries (as per World Bank standards). Finally, each country’s average 10-year inflation data is recorded. We assume that CB independence remains relatively static over time.

The results are shown below.

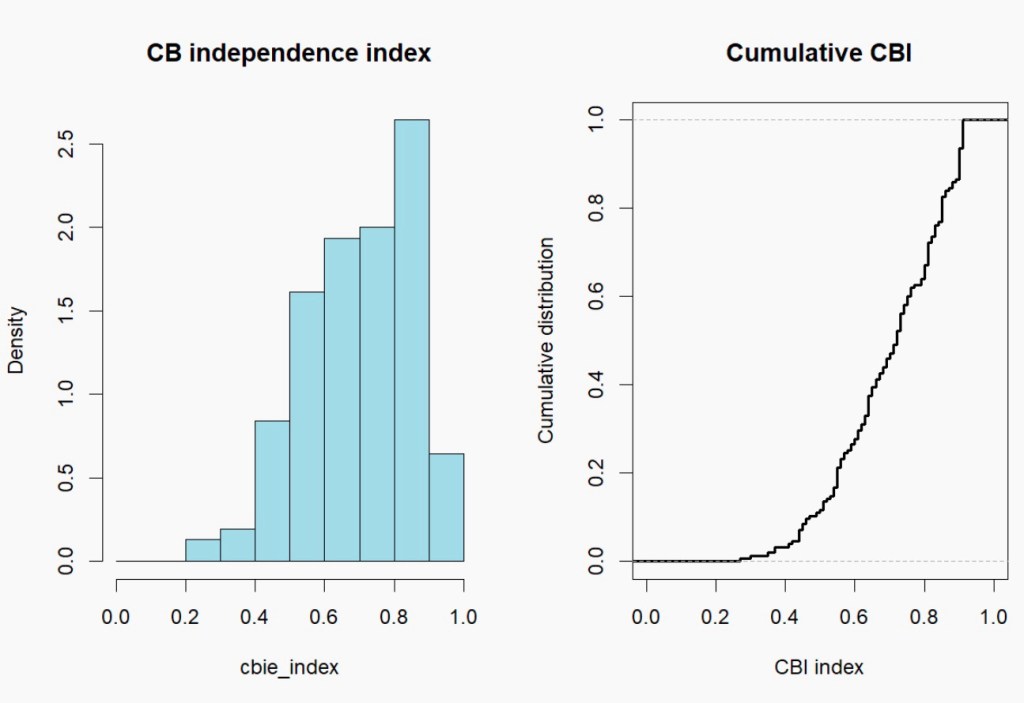

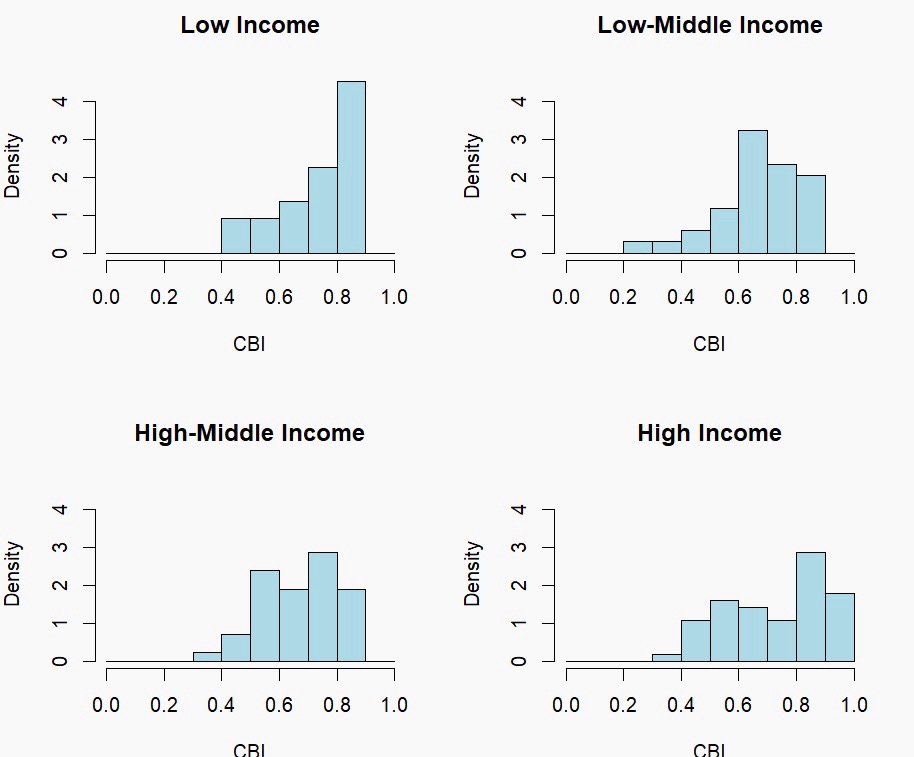

The distribution of central bank independence index values are mostly left-skewed, with most observations clustering around the 0.6 to 0.9 mark. Surprisingly, low-income countries feature the highest average scores of CB independence, also featuring the lowest variability. The highest median is attributed to high-income countries. The expected positive relationship between income level and CB independence only takes form beginning with low-middle-income countries.

Indeed, a regression on CB independence against economic development reports statistically significant results implying that middle-income countries predict marginally lower independence scores than their high-income counterparts.

Next, for the most interesting part of the analysis. The focus is now on addressing the central question of whether stronger central banking institutions correlate with better inflation outcomes. Better and lower are used synonymously here.

Interestingly, the correlation between average rates of inflation and central bank independence is negative for all except for high-income countries. The negative relationship is strongest for low-income countries, with middle-income countries featuring weakly negative correlations. Indeed, the steepest line when plotting the two variables corresponds to low-income group countries (shown below). This may point to independence being a significant factor in managing inflation only when overall economic institutions are weaker.

To better evaluate the link between our variables, I take a simple linear regression model that plots log average inflation (to smooth out large outliers) against the CB independence index. Economic intuition forces us to note that omitted variable bias is high, as with any bivariate regression. Inflation outcomes are of course reflective of greater trends than CB independence. The results may nevertheless be indicative of real relationships.

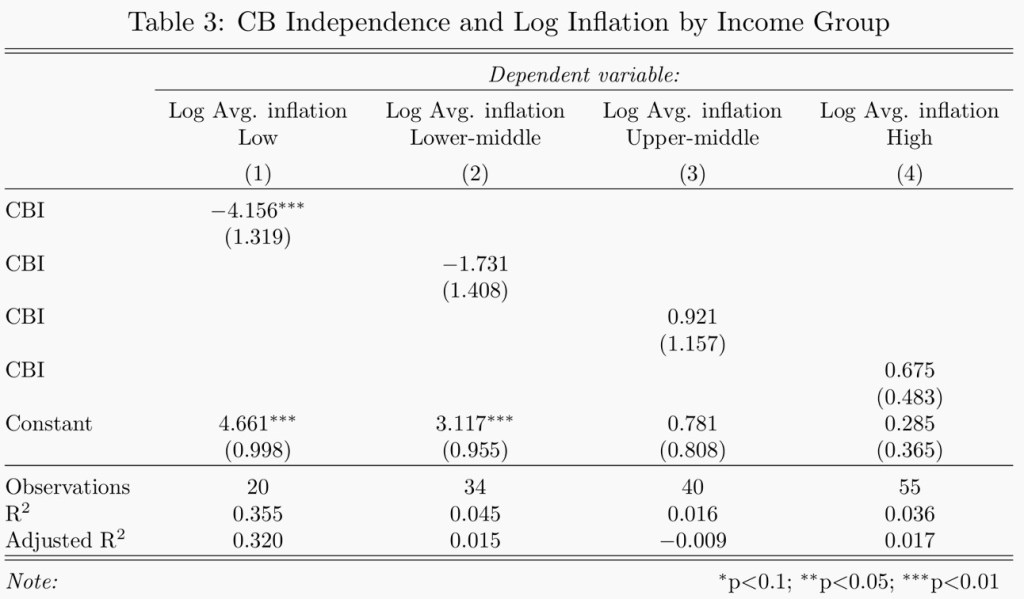

Whilst an aggregate model with all countries proves not to be useful, building four regressions applied separately to each income group does give interesting results. CBI becomes a statistically significant predictor of average inflation in low-income countries: the simple model predicts that a 0.1 unit increase in the independence index of a low-income country is associated with a

or 34% fall in average 10-year inflation figures. Cool! This aligns with low-income countries also having featured the strongest negative slope in the correlation table. Indeed, it appears that CB independence has its strongest economic effect when other surrounding institutions are weaker. A note is that, despite the strong statistical significance, the low observation count adds fragility to the results.

To sum up, as implied by the distributions, middle income countries do indeed feature comparatively lower independence scores. Central bank independence, however, was only shown to be economically significant for low-income countries, where a strong link emerged between independence and positive inflation outcomes. We conclude that economic development is associated with stronger central banking institutions, but independence itself loses its strong surface-level economic effect given an environment of better institutions across the board.

I will try to not use regressions in the next post. Try.

Leave a comment